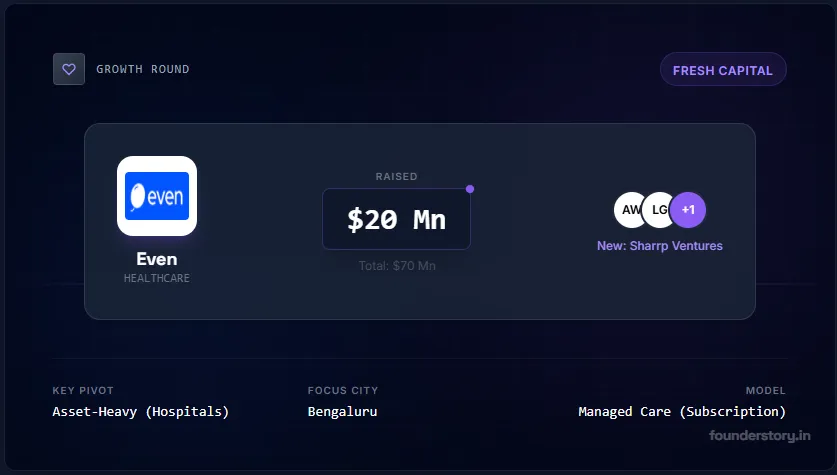

Even Healthcare has secured a fresh $20 million (₹180.5 crore) funding round, signaling a robust vote of confidence in its contrarian "managed care" model. The round saw participation from existing heavyweights like Lachy Groom and Alpha Wave, alongside new entrant Sharrp Ventures.

This latest injection brings the startup's total funding to $70 million. Unlike typical health-tech players that focus on insurance aggregation or tele-consults, Even is taking the harder path: owning the entire healthcare delivery stack, including physical hospitals.

FounderStory Intelligence

From Insurance to Infrastructure

Founded in 2020, Even started with a unique proposition: a subscription model that covers unlimited doctor consultations and diagnostics, removing the per-visit cost anxiety for patients. Unlike traditional insurance which kicks in only during hospitalization, Even covers everyday health needs (OPD).

Now, they are taking a massive leap into infrastructure. The startup plans to utilize the fresh capital to expand its hospital footprint in Bengaluru. This follows the launch of their first hospital in the city in May 2025.

The "Managed Care" Thesis

Even is effectively building an Indian version of Kaiser Permanente—a US-based giant that combines insurance with hospital ownership. By owning the hospitals, Even can control costs, ensure quality of care, and focus on preventative health rather than just sick-care.

This model aligns incentives perfectly: because Even pays for the care from the subscription fee, it is financially beneficial for them to keep their members healthy, rather than perform unnecessary surgeries.

FounderStory Takeaway

The shift from "Asset-Light" to "Full-Stack" is the defining trend of 2025-26 in Indian health-tech. Investors are realizing that you cannot fix healthcare purely with software. Even Healthcare's move to build hospitals is bold and capital-intensive, but if executed well, it creates a formidable moat that pure-play insurers cannot breach.